To ensure your strata building has adequate insurance protection, your Strata Manager engages a specialist insurance broker to obtain the most suitable Strata Insurance policy. When it comes to protecting the interior of a unit however, the onus falls on both unit owners and tenants.

As an owner-occupier, landlord or tenant, are you aware of the insurance policies you need?

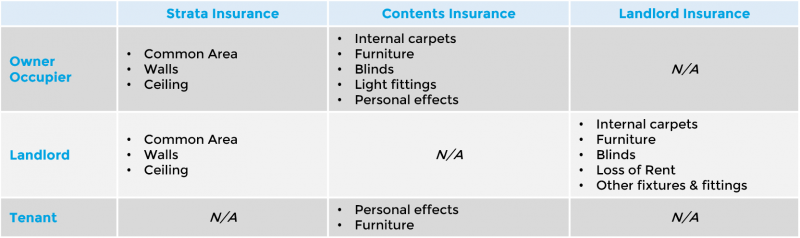

Strata Insurance policies exclude certain fixtures and general contents within individual units (e.g. carpets, curtains, blinds, light fittings and un-fixed electrical appliances). Accordingly, it is essential for strata unit owners and tenants to cover these items for their full value under Landlords or Contents Insurance.

Landlords Insurance for Strata Unit Owners

If you lease out your unit, ensure your investment property is protected with a comprehensive Landlord Insurance policy.

Landlord Insurance is designed to cover:

- loss of rent

- rent default

- malicious damage by a tenant or third party

- legal liability cover should a tenant sustain an injury within the property

- fixtures and fittings e.g. carpets, blinds and light fittings (excluded under a Strata policy)

With appropriate coverage, you can rest assured that your rental income and property can be protected from significant financial loss.

What level of cover should a Landlord have?

While different insurers provide varying cover, Whitbread generally recommend that strata unit owners purchase Accidental Damage Landlords cover to protect against a wide range of insurable events and losses that could occur.

The alternative, Defined Events cover, only offers protection against a narrow range of specified events (typically fire and weather-related causes i.e. storm, lightning, earthquake, cyclone), and may fail to cover you in the event of a claim.

Contents Insurance for Owner-occupiers & Tenants

If you are an owner-occupier or tenant living in a strata unit, it is essential to have Contents Insurance.

Contents Insurance can offer protection against:

- loss or damage to the contents and valuables inside a dwelling for a variety of causes e.g. fire, storm, theft, accidental damage

- malicious acts caused by a third party e.g. deliberate damage to furniture, certain fixtures and fittings, and carpets (if owner-occupied)

- third party liability claims e.g. a guest who trips and sustains an injury while climbing stairs

It is essential that owner-occupiers and tenants protect their personal items and liability exposures under a Contents policy, as these are not covered by a Strata Insurance policy.

Examples of items covered by Contents Insurance

Contents Insurance generally covers household and personal possessions such as clothing, jewellery, furniture, TVs, computers, internal carpets, blinds and electrical appliances (where such appliance are not covered by a Landlords policy). There are some specific high-end items (e.g. expensive jewellery and artwork) that may be excluded under a standard Contents Insurance policy. Policy holders need to be diligent to ensure their insurance policy extends to provide cover for these items where necessary.

Underinsurance is common

If you have recently sold or purchased any expensive items, your Contents Sum Insured may no longer reflect the true value of your belongings.

Owner-occupiers and tenants must re-evaluate their Contents Sum Insured annually (at least) to ensure that any additional contents, especially high-value items, have either been included in their Sum Insured or noted on their insurance policy.

Remaining vigilant and making the necessary adjustments to your Contents policy is the best way to avoid underinsurance and hefty financial losses in a claim.

Unsure how to calculate a correct Contents Sum Insured?

If you are unsure how much you should insure your contents for, Steadfast have introduced a Contents Sum Insured calculator* to help you get a more accurate estimate. Simply click here.

Examples of what each policy can cover in a claim:

Looking for an easy online solution?

In partnership with CHU Underwriting Agencies Pty Ltd, Whitbread is offering online Contents and Landlords Insurance solutions to help strata unit owners and tenants avoid gaps in cover. Simply click the relevant button to get your online quote:

For more information on Landlords or Contents Insurance, submit an online enquiry form or speak to a Whitbread insurance broker:

T | 1300 424 627

E | info@whitbread.com.au

This article is not intended to be personal advice and you should not rely on it as a substitute for any form of personal advice. Please contact Whitbread Associates Pty Ltd ABN 69 005 490 228 Licence Number: 229092 trading as Whitbread Insurance Brokers for further information or refer to our website.

*Typical building contents replacement costs are provided by Sum Insured Pty Ltd (A.B.N. 55 947 630 521 (‘SI’) trading as Home Contents. Whilst every care is taken to ensure the accuracy of the information as a guide for costing, no responsibility is accepted by SI, Steadfast or the Steadfast Broker for its accuracy. Please check with a Valuer or other suitably qualified professional for an accurate estimate. Neither Steadfast nor the Steadfast Broker takes any responsibility for the costs provided by SI, or any liability for the accuracy of or reliance upon or use of, the costs. To the fullest extent permitted by law, SI, Steadfast and the Steadfast Broker expressly disclaim all warranties, express or implied, including, but not limited to, the implied warranty of fitness for a particular purpose. SI, Steadfast and the Steadfast Broker do not warrant or make any representations regarding the use or the results of the use of the information provided in terms of its correctness, accuracy, reliability, or otherwise.